Cash App Launches ‘Pay Later’ for P2P Transfers

Cash App’s new buy now, pay later option for person-to-person payments rewrites the rules of instant money—and your credit score is the next card on the table.

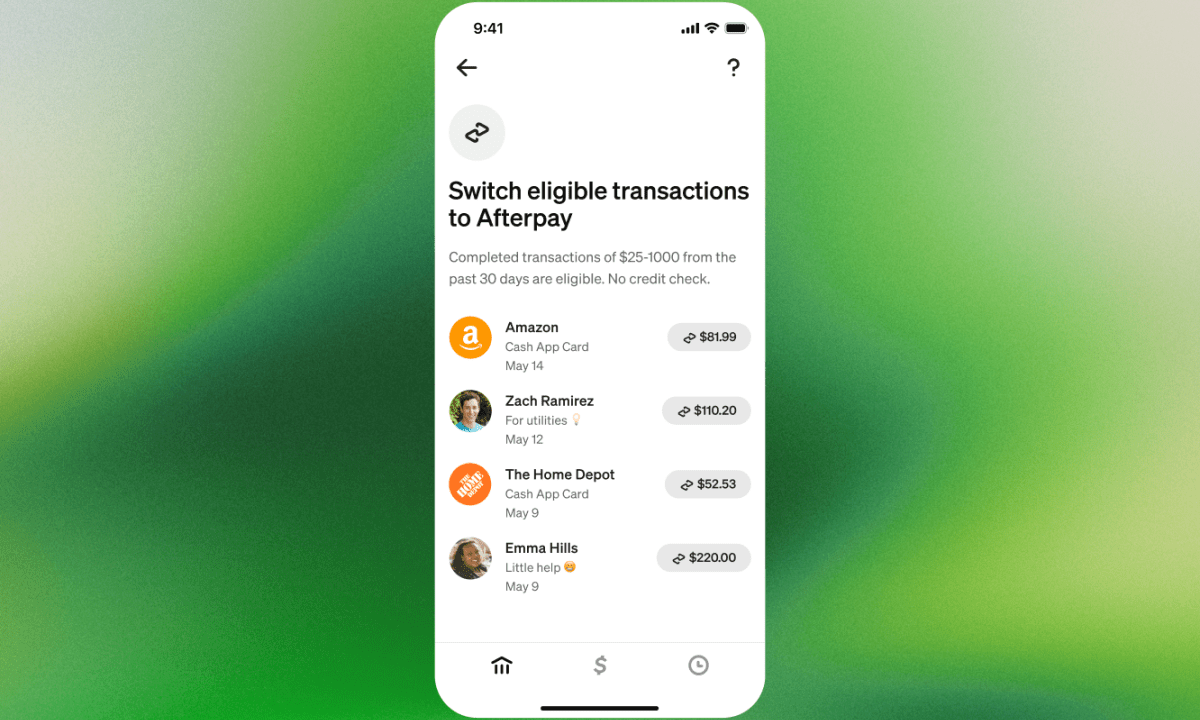

Cash App has officially rolled out a “pay later” feature for peer-to-peer transfers, letting users send money to friends or family without pulling from their own balance immediately. Instead, the app fronts the cash, and the sender repays in installments. This move blurs the line between social payments and short-term credit, introducing a BNPL (buy now, pay later) dynamic to the informal world of splitting dinner tabs, rent, or birthday gifts.

The feature works like a mini loan: when you send money to another Cash App user, you can opt to pay in four equal biweekly installments, interest-free—provided you make all payments on time. If you miss a payment, late fees apply, and the debt can be sent to collections. This is not a credit card or a bank overdraft; it’s a new category of instant consumer credit embedded inside a money-transfer app.

For Cash App, the strategic value is twofold. First, it keeps users inside the app longer. Instead of hitting a “send” button and leaving, users now have a repayment schedule, reminders, and recurring engagement. Second, it creates a new revenue stream: merchant fees from BNPL have been lucrative for Afterpay and Klarna, but Cash App is applying the same model to interpersonal transfers—a market that has never before carried a financing layer.

For users, the appeal is obvious. You can cover a friend’s emergency vet bill or chip in for a group gift without waiting for your next paycheck. The friction of “I’ll pay you back later” is replaced with a structured, digital IOU. But the hidden cost is behavioral. BNPL products are known to encourage overspending because the pain of payment is delayed. When the “pain” is also social—your friend expects the money now—the psychological pressure to send funds you don’t have could spike.

The credit aspect adds another layer. Cash App says it will report missed payments to credit bureaus. That means an unpaid “pay later” transfer could ding your credit score, even if the original amount was as small as $20. The feature essentially turns every P2P send into a potential credit event. Users under 18 cannot use it, and approval is subject to a soft credit check, but no hard inquiry is performed upfront.

This launch also signals a broader shift in how fintechs view cash flow. Instead of treating P2P as a utility—fast, free, forgettable—Cash App is transforming it into a financial product with stickiness and risk. It positions the app closer to a digital bank, offering credit-like services without the regulatory overhead of a bank charter.

Competitors like Venmo and Zelle have not yet added BNPL for personal transfers, though Venmo offers a credit card with buy now, pay later for purchases. Cash App’s move could pressure others to follow, especially as younger users increasingly prefer flexible payment options over traditional credit cards.

The practical takeaway for consumers: “pay later” is a convenient tool for short-term liquidity crunches, but treat it like a loan, not a gift. Set reminders, automate repayments, and avoid using it for routine expenses. One missed $10 payment can cost more in late fees and credit damage than the original transfer.

Cash App is monetizing your next “I’ll pay you back.” Whether that’s a lifeline or a trap depends on how you pay yourself back. Use the feature to bridge a gap, not to create one.

No Comments